HOUSTON: A number of key Texas refineries worked to reopen or resume normal operations on Saturday, a week after Hurricane Harvey knocked out nearly one quarter of the US refining capacity and sent gasoline prices to two-year highs.

While much of the region’s refining infrastructure still remained offline from Harvey, which made landfall as a Category 4 hurricane last week and drenched Texas as a tropical storm, the restarts were a first step in alleviating concerns about US fuel supplies.

Exxon Mobil said it was restarting its 560,500 barrel per day (bpd) facility in Baytown, Texas, the second-biggest US oil refinery, after it was inundated by flooding.

Phillips 66 said it was working to resume operations at its 247,000 bpd Sweeny refinery as well as its Beaumont terminal.

The announcements come after Valero Energy said late on Friday it was ramping up production at its Corpus Christi, Texas-area refineries, as well as evaluating its 335,000 bpd Port Arthur, Texas, refinery for damage from Harvey. The refinery was shut on Wednesday.

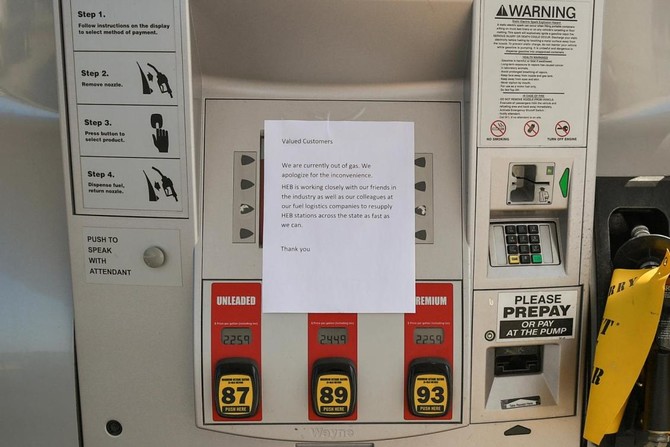

Retail gasoline prices have risen more than 17.5 cents since August 23, before Harvey hit, amid worries the storm would trigger supply shortages.

Pump prices were at $2.59 a gallon on Saturday, according to motorists advocacy group AAA, up 3 percent from Friday and 16.7 percent higher on average than a year ago.

In another positive sign for the industry, Occidental Petroleum said it had loaded and shipped the first crude cargo from its Ingleside terminal in Corpus Christi after Hurricane Harvey first made landfall.

The Port of Corpus Christi, a major energy industry shipping hub, was partially open and hoped to resume normal operations next week, officials said.

But much energy infrastructure remained offline, including the largest US refinery, the 603,000 bpd facility in Port Arthur, Texas, owned by Motiva Enterprises. Motiva has told customers to prepare for fuel shortages, said a source at convenience store and gas station chain Circle K.

In some Texas cities, including Dallas, there were long lines at gas stations on Friday.

At a QMart filling station west of Houston on Saturday, cars were clogging the pumps soon after a tanker arrived to replenish its pumps.

“We had a half a tank, but decided to get more, just in case,” said Maria Linares, a school teacher whose husband was topping their car’s tank.

The Phillips 66 brand station has not raised its fuel prices since before Harvey, said Assistant Manager Jalal Sadruddin, by policy of the station owner, Q-Mart.

“Right now, we have about 4,000 gallons, maybe two or three days’ worth,” he said. The station received a tanker load of gasoline on Saturday but was out of diesel, he said. An Exxon brand station across the street was out of fuel.

“In all this area, no one has it but us,” Sadruddin said.

Nearly half of US refining capacity is in the Gulf Coast region, an area with proximity to plentiful supplies from Texas oil fields to Mexican and Venezuelan oil imports. The majority of Texas ports remained closed to large vessels, limiting discharge of imported crude.

Texas refineries begin restart after hit from Hurricane Harvey

Texas refineries begin restart after hit from Hurricane Harvey

Saudi Arabia raises $628m in June sukuk offering

JEDDAH: Saudi Arabia’s National Debt Management Center has completed its June issuance under the government’s riyal-denominated sukuk program, raising SR2.355 billion ($628 million).

The figure marks a decline of 42 percent from May’s SR4.08 billion, which was the highest monthly total recorded this year. The drop reflects typical fluctuations in the government’s monthly funding activity.

The June offering was divided into five tranches. The first amounted to SR25 million and will mature in 2027. The second, totaling SR1.175 billion, will mature in 2029. The third tranche stood at SR500 million and is set to mature in 2032. The fourth was SR5 million, maturing in 2036, while the fifth and final tranche reached SR650 million, due in 2039.

Sukuk, which are structured to comply with Islamic finance principles, offer investors returns generated from tangible assets or projects, rather than traditional interest payments. These instruments continue to attract strong demand from investors seeking stable, Shariah-compliant returns.

Despite the month-on-month decline, the latest issuance underscores Saudi Arabia’s efforts to diversify its funding base and develop the domestic debt market.

The NDMC has maintained a steady pace of monthly issuances this year, including SR3.72 billion in January, SR3.07 billion in February, SR2.64 billion in March, and SR4.08 billion in May.

Saudi Arabia continues to lead the Gulf Cooperation Council in sukuk and bond activity. In the first quarter of 2025, the Kingdom accounted for more than 60 percent of all primary debt issuances in the region, raising $31.01 billion from 41 offerings, according to the Kuwait Financial Center, known as Markaz.

In a broader outlook, S&P Global has highlighted Saudi Arabia’s expanding non-oil economy and strong sukuk activity as key drivers for growth in global Islamic finance.

The agency forecasts total sukuk issuance could reach between $190 billion and $200 billion in 2025, with up to $80 billion in foreign-currency issuances, assuming stable market conditions.

Looking ahead, Kamco Invest projects that Saudi Arabia will lead the GCC in bond maturities over the next five years. Between 2025 and 2029, about $168 billion in Saudi bonds are expected to mature, underscoring the Kingdom’s prominent role in the region’s debt landscape.

Closing Bell: TASI rises 2.37% to close at 10,964

RIYADH: Saudi Arabia’s Tadawul All Share Index rose 254.04 points, or 2.37 percent, to close at 10,964.28 on Tuesday.

Total trading turnover reached SR8.48 billion ($2.26 billion), with 248 stocks posting gains and five declining.

The Kingdom’s parallel market Nomu also recorded an increase, gaining 492.72 points, or 1.87 percent, to settle at 26,850.79, as 73 stocks advanced and 22 retreated.

The MSCI Tadawul 30 Index, meanwhile, gained 29.06 points, or 2.11 percent, to finish at 1,406.69.

Red Sea International Co. was the best-performing stock of the session, with its share price rising 9.97 percent to SR42.45. Salama Cooperative Insurance Co. followed with a 9.92 percent increase to SR13.52.

Other gainers included Saudi Cable Co., which rose to a fresh year high on Tuesday, closing at SR147.20 with a 6.05 percent increase.

On the losing side, SABIC Agri-Nutrients Co. saw the steepest decline, falling 4.58 percent to SR104.2. Saudi Arabian Oil Co. dropped 1.62 percent to SR24.34, and Taleem REIT Fund declined 0.85 percent to SR9.30.

Dar Al Arkan Real Estate Development Co. announced its intention to issue a dollar-denominated, fixed-rate, Shariah-compliant sukuk under Regulation S, as it seeks to broaden its funding base and support general corporate purposes.

The Riyadh-based property developer has appointed a consortium of regional and international banks to act as joint lead managers and bookrunners for the issuance.

These include Abu Dhabi Commercial Bank, Abu Dhabi Islamic Bank, and Alkhair Capital, as well as Al Rayan Investment and Arqaam Capital. Other participants are Bank ABC, Dubai Islamic Bank, Emirates NBD Capital, and First Abu Dhabi Bank.

The list also features J.P. Morgan, Mashreq, and Sharjah Islamic Bank, as well as Standard Chartered Bank, and Warba Bank.

The appointed banks will arrange a series of fixed income investor calls starting June 24, ahead of the planned sukuk offering in global capital markets.

The transaction remains subject to market conditions and regulatory approvals, including compliance with Financial Conduct Authority and International Capital Market Association stabilization rules.

The offering is classified as a benchmark senior unsecured sukuk under Regulation S, which allows for international placement with institutional investors. The value of the sukuk will be determined based on market conditions at the time of issuance.

According to the company’s statement on Tadawul, the proceeds from the issuance will be used for general corporate purposes. The board of directors approved the sukuk issuance on May 29.

Dar Al Arkan’s share price closed the session 2.70 percent higher to reach SR19.

Oman’s sovereign fund nets $4.1bn profit with disciplined, future-focused strategy: Report

- OIA ranked 35th globally by assets under management among sovereign wealth funds

- Around 61.3% of its portfolio is invested locally

RIYADH: Oman’s sovereign wealth fund posted a record profit of 1.59 billion Omani rials ($4.1 billion) in 2024 and grew its assets above 20 billion rials, Global SWF reported.

The additional revenue enabled the Oman Investment Authority to transfer 800 million rials into the national budget, according to the report, providing a vital fiscal cushion and underscoring the fund’s expanding dual role as both an economic engine and a diplomatic asset.

Beyond headline profits, OIA is executing a strategic shift, prioritizing domestic investments to generate local value while forming global partnerships to secure future-ready capabilities in areas such as artificial intelligence, clean energy, logistics, and manufacturing.

Ranked 35th globally by assets under management among sovereign wealth funds, the OIA is increasingly being viewed as a nimble but ambitious player.

According to Global SWF, its disciplined portfolio strategy, increased transparency, and joint fund architecture are transforming the fund into a networked sovereign investor with a growing international footprint.

At home, OIA’s economic impact is significant. Around 61.3 percent of its portfolio is invested locally, mainly through its National Development Fund, which exceeded its 2024 target by deploying 2.1 billion riyals in strategic projects, according to Global SWF.

These include infrastructure ventures such as the Duqm Refinery, new mining operations in Lasil and Al Baydha, and solar energy plants in Manah.

Over the past year, the fund has inked a $300 million joint investment platform with Algeria and expanded its Vietnam-Oman Investment Fund.

These investments signal a shift in Gulf sovereign wealth funds— from passive holdings to active, technology-driven deal-making aligned with national objectives.

In parallel, OIA has launched the Future Fund Oman with an allocation of $5.2 billion, targeting large-scale domestic projects, small and medium-sized enterprises, and startups, according to a separate May report by Global SWF.

In its first year, the fund approved over $2 billion in deals, with 75 percent of capital coming from foreign investors, underlining investor confidence in Oman’s diversification agenda.

Investing for Vision 2040

OIA’s 2024 performance also reflected its focus on human capital and job creation, with nearly 1,400 new roles generated and the Omanization rate across OIA-linked entities reaching 77.7 percent.

Through programs like Jadarah, Nomou, and Eidaad, the fund is aligning education, training, and employment with Vision 2040’s long-term growth objectives.

Meanwhile, the fund is moving from asset accumulation toward strategic exits. Since 2022, it has divested 19 assets, including three major IPOs: Abraj Energy Services, OQ Gas Networks, and Pearl REIF— raising over $2.5 billion, according to the release.

The October listing of 25 percent of OQ Exploration & Production marked Oman’s largest-ever IPO, signaling deepening liquidity in Muscat’s capital markets, according to the Global SWF May report.

OIA’s roadmap includes 30 more divestments through 2029 across sectors, including logistics, utilities, and aquaculture, aiming to crowd in private capital and raise governance standards. These IPOs are structural tools to deepen Oman’s market while supporting the transition to a knowledge-based economy.

Global investment, local value

Even as it expands abroad, OIA insists every foreign investment must deliver back home— whether in skills, supply chain resilience, or technology transfer. Recent deals illustrate this ethos.

In the US, OIA invested in Tidal Vision, a company developing climate-smart biopolymers. In Singapore, it joined a $100 million venture capital fund with Golden Gate Ventures and helped establish a Muscat-based venture office to incubate deep-tech startups.

In one of its most high-profile moves, OIA took a stake in Elon Musk’s xAI, joining fellow Gulf players like Saudi’s Kingdom Holding and Qatar Investment Authority.

The move links Omani capital to frontier technology while reinforcing the fund’s mandate to back high-potential sectors shaping the global economy.

The OIA’s operational discipline has not gone unnoticed. Since 2021, it has reduced its subsidiary debt by nearly $5.6 billion, standing at $23.92 billion as of the end of the third quarter of 2024. It also refused to issue any new government guarantees last year, according to Global SWF, boosting investor confidence. Ratings agency S&P cited OIA’s reforms and transparency in reaffirming Oman’s BBB- rating with a positive outlook.

Mawani names Al-Mazroua as new president

JEDDAH: Saudi Ports Authority has appointed Suliman bin Khalid Al-Mazroua as its new president, effective June 29, as part of its push to strengthen leadership and advance key strategic goals.

Al-Mazroua succeeds Mazen bin Ahmed Al-Turki, who had been serving as acting president and played a key role in several initiatives aimed at developing logistics zones and parks across the Kingdom.

Al-Turki’s most recent contribution included overseeing the signing of a series of new build-operate-transfer contracts valued at more than SR2.2 billion ($586.6 million) to develop multi-purpose cargo terminals at eight Saudi ports.

The appointment of Al-Mazroua, announced by Mawani’s board of directors, underscores the authority’s commitment to supporting the National Transport and Logistics Strategy and Saudi Vision 2030. Both initiatives aim to position the Kingdom as a global logistics hub and a leading industrial power.

In a post on his X account, Al-Mazroua expressed his appreciation for the board’s trust and pledged to further the authority’s strategic goals.

“I extend my sincere thanks and appreciation to His Excellency the Minister of Transport and Logistics Services and Chairman of the Board of the Saudi Ports Authority, Eng. Saleh bin Nasser Al-Jasser, as well as to their Excellencies and distinguished members of the board for this generous trust,” he said.

Al-Mazroua added: “I pray to God for success in serving our blessed country and fulfilling the aspirations of our visionary leadership. I am also very pleased to work alongside my colleagues at the Saudi Ports Authority.”

In a statement, the authority said that Al-Mazroua “affirmed his commitment to advancing Mawani’s strategic objectives and enhancing its performance in line with its development plans and transformation programs.”

Before assuming his new role, Al-Mazroua served as CEO of the National Industrial Development and Logistics Program, where he played a key role in driving economic diversification and enhancing infrastructure in key sectors, including industry, mining, energy, and logistics.

“He also played a key role in stimulating investment in these sectors with the aim of increasing their contribution to the Kingdom’s gross domestic product, promoting innovation, enhancing local content, and advancing the Fourth Industrial Revolution,” the statement added.

With more than two decades of professional experience, Al-Mazroua has held several senior leadership positions, including at Saudi Aramco from 2001 to 2017.

Over the years, he progressed from technical roles to executive leadership, contributing to the establishment of research and development centers, strengthening cybersecurity frameworks, and advancing health care sector initiatives.

He also worked at US-based Aruba Networks from November 2006 to July 2007 and previously served as a quality assurance engineer at California-based Caspian Networks.

In addition, Al-Mazroua led the National Transformation Program and the Delivery and Rapid Intervention Center, where he contributed to planning, monitoring, and accelerating the implementation of development initiatives in support of Vision 2030.

He is also a member of several boards, including the Center for the Fourth Industrial Revolution in Saudi Arabia and Marafiq Co.

Saudi Arabia, Bahrain launch 2nd phase of industrial integration

RIYADH: Saudi Arabia and Bahrain have launched the second phase of their industrial integration initiative, aiming to boost bilateral trade, investment, and cross-border supply chain cooperation.

Announced on the sidelines of the Saudi Industry Forum 2025 in Dhahran, Khalil Ibn Salamah, the Kingdom’s deputy minister for industrial affairs, emphasized that the new phase would build on prior successes between the two countries.

This comes amid strengthening economic ties between the countries, with the Saudi Arabia’s direct investments in Bahrain reaching SR35 billion ($9.33 billion) in 2023 — representing approximately 20 percent of total foreign investments — and 1,550 Saudi-registered companies operating in the country, as revealed by the Kingdom’s Minister of Investment, Khalid Al-Falih, during a business forum earlier this year.

In an official statement marking the latest announcement, the Saudi Ministry of Industry and Mineral Resources stated: “The second phase of industrial integration between the two countries focused on setting specific targets, including enhancing intra-trade in industrial goods, attracting industrial investments.”

It added that this will help “integration in the field of industrial infrastructure and supply chain integration,” as well as identifying a list of export opportunities for non-oil goods and facilitating procedures for exporters and investors.

The initiative is part of broader efforts under the Gulf Cooperation Council Economic Agreement, which aims to increase the industrial sector’s contribution to regional GDP and foster industrial coordination among member states “on an integrated basis,” according to the ministry.

The second phase builds on earlier efforts, including the Future Factories Program, which helped shift production in both countries from labor-intensive to advanced manufacturing, along with aligning policies to treat local products as national goods and streamline customs processes.

As part of the second-phase launch, Ibn Salamah inaugurated the Bahraini Investors Services Office in Dammam’s Third Industrial City. The event was attended by Bahrain’s Minister of Industry and Commerce, Abdullah bin Adel Fakhro.

“The office aims to attract quality industrial investments and provide all industrial investment services to investors,” the ministry noted.

Positioned strategically near Bahrain, approximately 130 km away, Dammam’s Third Industrial City offers a robust industrial ecosystem.

Spanning 48 million sq. meters, the site features extensive infrastructure including a modern road network, energy and water supply systems, and logistical connectivity through its proximity to King Fahd Port, King Fahd International Airport, and the dry port in the city of SPARK.

The Saudi Industry Forum also highlighted how the new office will offer a “package of services and enablers from the industrial and mining system to facilitate the journey of Bahraini investors,” further underscoring both countries’ commitment to deepening industrial and economic ties.