DEAD SEA, Jordan: Saudi Arabia’s startup scene is “moving faster than anyone can imagine” and is set to create hundreds of thousands of jobs over the coming years, the World Economic Forum in Jordan heard on Saturday.

The region’s most successful tech ventures — like ride-hailing service Careem, which Uber recently agreed to buy for $3.1 billion, and web portal Maktoob, which was acquired by Yahoo in 2009 — have emerged from more established startup hubs of Dubai and Amman.

But the next wave is seen emerging from Saudi Arabia, panelists said at the regional meeting of the World Economic Forum (WEF) at the Dead Sea.

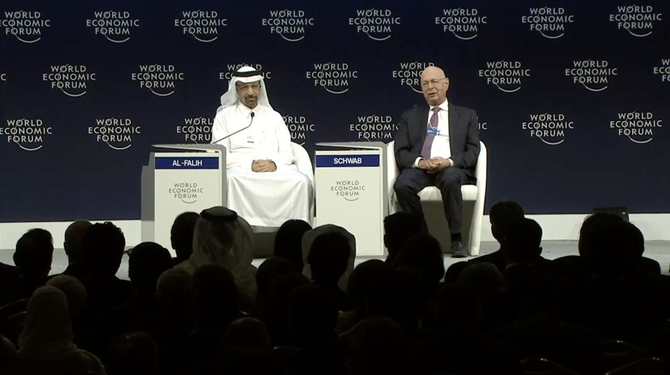

Saudi Arabia’s Energy Minister Khalid Al-Falih told the forum that he expects the startups of today to be among the Kingdom’s biggest companies in a decade’s time.

“Our enterprises will multiply in size,” he said. “I predict that by 2030, companies that we don’t know today will be among the top 20, 30 companies in Saudi Arabia. They will be driven by innovation, they will be driven by young people, they will be driven by women.”

The government has a role to play in encouraging more Saudi startups, along with a culture where young people experiment in business, the minister added.

“(It’s about) creating an environment where failure is not encouraged, but certainly dealt with in a positive way — and that young people are given the opportunity to fail, fail, fail, and succeed ultimately, and not only create opportunities for themselves … but also employment and opportunities for hundreds of thousands of people.”

Al-Falih pointed to the venture capital funds and startup incubators that are already active in the Kingdom.

“We hope to see hundreds of these startups coming up with innovations that are not only going to change our countries in the region, but indeed in due course will be part of the global movement where young, innovative enterprises are creating the economies and the solutions of the future,” he said.

Ten Saudi companies made it to the WEF’s 100 most promising startups for 2019, with entrepreneurs from the Kingdom in attendance at the event.

Fadi Ghandour, the founder of courier service Aramex and executive chairman of venture capital firm Wamda Capital, said that the Kingdom’s startup scene has virtually transformed overnight.

“I am extremely impressed. Suddenly you thought nothing is happening, and then you wake up in the morning and you say ‘what happened here?’,” he told a panel at the event.

“Saudi Arabia is a country that is changing, it is moving faster than anybody can image … It’s an exciting time, it is where the region is going to scale its businesses.”

Ghandour was joined on the panel by Ayman Alsanad, co-founder and CEO Mrsool, the Saudi delivery app that recently received multi-million dollar investments from Saudi Technology Ventures and others.

Audrey Nakad, co-founder of the education platform Synkers, which is based in Lebanon, told the panel that her company is preparing to expand into Saudi Arabia. Synkers provides a link between tutors and students looking for additional help.

Thriving Saudi startup scene to produce top-30 companies, WEF hears

Thriving Saudi startup scene to produce top-30 companies, WEF hears

- Agile new businesses of today will be among Kingdom’s largest by 2030, World Economic Forum hears

- Khalid Al-Falih told the forum that he expects the startups of today to be among the Kingdom’s biggest companies

Egypt’s economy expands 4.3% in second quarter, says minister

RIYADH: Egypt’s economy grew 4.3 percent in the second quarter of 2024-25, accelerating from 2.3 percent a year earlier, driven by structural reforms and rising private sector investment, Planning Minister Rania Al-Mashat said.

The improved performance reflects the government’s fiscal and monetary adjustments alongside a reduction in public investment, which Al-Mashat said has helped stabilize the economy and drive growth.

The minister previously forecast 4 percent growth for the full fiscal year, highlighting Egypt’s focus on improving its investment climate and securing $4.2 billion in macroeconomic support from global partners.

In a statement posted on the government’s official Facebook page, she said: “This is driven by structural reforms aimed at diversifying sources of growth and increasing the competitiveness of the Egyptian economy, which was evident in the strong performance of productive sectors such as manufacturing, tourism, and communications.”

Al-Mashat added that the government is working to shift toward tradable sectors like manufacturing to create a more diversified and sustainable economy, strengthening Egypt’s ability to navigate global economic challenges.

She also highlighted the positive outlook for gross domestic product growth, supported by ongoing structural reforms and economic diversification.

Non-oil manufacturing led economic growth, expanding by 17.74 percent — a sharp turnaround from an 11.56 percent contraction in the same period last year — driven by increased production and faster customs clearance.

The tourism sector maintained its strong performance with an 18 percent surge, while private investment rose, making up more than half of total investments. Public investment, however, declined by 25.7 percent.

The Information and Communications Technology sector grew by 10.4 percent, supported by digital infrastructure expansion and rising demand for services.

Despite ongoing geopolitical tensions affecting Suez Canal activity and a slowdown in the extraction sector, Al-Mashat underscored that economic reforms remain key to building a more competitive, sustainable economy and bolstering investor confidence.

She noted that net exports turned positive in the second quarter, driven by growth in commodity and service exports.

In January, Al-Mashat reiterated the government’s focus on disciplined investment management, stating that the public investment budget for the year is capped at 1 trillion Egyptian pounds ($19.78 billion), prioritizing projects that are at least 70 percent complete.

Between 2020 and 2024, Egypt’s private sector secured $14.5 billion in concessional development financing from global partners. For the first time, private sector access to international soft financing surpassed that of the government in 2024, Al-Mashat noted at that time.

She also revealed that negotiations are ongoing with the EU and other international partners for a second phase of macroeconomic support, including €4 billion ($4.10 billion) in budget aid and €1.8 billion in investment guarantees.

CMA proposes easing investor criteria for Nomu to boost participation, liquidity

JEDDAH: Saudi Arabia’s Capital Market Authority has proposed easing investor criteria for Nomu, the Kingdom’s parallel market, aiming to expand participation and improve liquidity.

The proposed amendments suggest reducing the minimum transaction requirement for individual investors from SR40 million ($8 million) to SR30 million over a 12-month period.

Additionally, the requirement for quarterly trading activity would be eliminated. Under the new regulations, board and committee members of companies listed on Nomu would also be eligible to qualify as investors.

The project aims to reserve the term “Qualified Investor in the Parallel Market” for eligible categories, amend the minimum transaction value required for classifying a natural person as a qualified investor, and rank board members and committee members of listed companies as suitable to invest.

Saudi Arabia accounted for 31 percent of the region’s total initial public offering proceeds in 2024, making it the second-largest contributor after the UAE. The Saudi Exchange, Tadawul, witnessed 14 IPOs on its main market, collectively raising $3.8 billion. Nomu also saw 28 IPOs, generating $297 million.

The CMA called upon relevant and interested persons participating in the capital market to share their feedback on the draft for 30 days, ending on April 28.

Earlier in March, the CMA called for feedback on the draft “Regulatory Framework for Debt Instruments Offering Platforms and Investing in Them,” which aims to develop debt instrument offerings by licensed capital market institutions for securities crowdfunding.

With the consultation period to end on April 23, the draft outlines regulatory and licensing requirements for offering and investing in debt instruments, aligning with developments in the capital market.

Key proposals include allowing organizations to present debt instruments in the sukuk and debt market and enabling companies with a FinTech Experimental Permit to obtain the necessary license to operate as capital market institutions.

Organizations will need an arranging license to offer debt instruments through crowdfunding platforms. The draft also introduces requirements for safeguarding client funds and registrable functions for licensed establishments.

The proposal aims to expand the role of capital market institutions in financial technology, enhance the debt market, and increase participation in securities crowdfunding, supporting the CMA’s objectives.

Jewelry spending fuels Saudi POS surge for 2nd consecutive week

RIYADH: Saudi Arabia’s point-of-sale transactions climbed 6.3 percent to SR14.4 billion ($3.8 billion) in the week ending March 22, with jewelry once again leading the growth.

The latest figures from the Saudi Central Bank, also known as SAMA, showed that spending in the sector registered the largest increase in the value of transactions at 29.9 percent to reach SR544.4 million.

Jewelry also saw a 34.4 percent surge in terms of the number of transactions, reaching 403,000.

The hotel sector ranked second with a 24.8 percent surge in transaction value to SR440 million. Spending on clothing and footwear followed, rising 24.5 percent, holding the second-largest share of POS transactions at SR1.87 billion.

Overall transactions increased by 22.4 percent to 12 million.

Expenditure on transportation edged up by 6.9 percent to SR950.8 million, and spending in restaurants and cafes increased by 3.7 percent, bringing the total value of transactions to SR1.5 billion.

The smallest spending increases were in the telecommunication and the construction sectors, rising by 0.2 percent to SR114.8 million and 0.03 percent to SR308 million, respectively.

Spending on education saw the steepest decline for the second week in a row, dropping 37.2 percent to SR88.2 million, following a 144.6 percent surge during the week from March 2 to 8 as students returned from the winter break.

Expenditure on public utilities saw a 4.5 percent dip to SR52.4 million, and spending on food and beverages recorded a 2 percent drop to SR1.88 billion, but still held the largest share of the POS.

Miscellaneous goods and services accounted for the third biggest POS share, with a 5.8 percent uptick, reaching SR1.7 billion.

Spending in the leading three categories accounted for approximately 38.1 percent, or SR5.5 billion, of the week’s total value.

Geographically, Riyadh dominated POS transactions, representing around 34.1 percent of the total, with spending in the capital reaching SR4.9 billion — a 4.6 percent increase from the previous week.

Jeddah followed with a 9.8 percent increase to SR2.1 billion, and Makkah came in third at SR933.2 million, up 14 percent.

Tabuk experienced the smallest increase in spending, edging up by 0.6 percent to SR248.2 million.

Buraidah and Makkah saw the largest increases in terms of number of transactions, surging by 4.2 percent and 3 percent, respectively, to 4.4 million and 9.8 million transactions.

Emirates NBD teams up with BlackRock to expand private market access

RIYADH: Dubai’s Emirates NBD has partnered with US-based investment firm BlackRock to launch a dedicated platform aimed at giving its wealthy clients greater access to private markets and alternative assets.

The two firms signed a memorandum of understanding to create this platform, as well as introduce an initial range of evergreen offerings focused on income and growth strategies, tailored exclusively for the UAE wealth market, according to a press statement.

Clients of Emirates NBD Asset Management will gain access to BlackRock’s Alternative Investments platform, which currently oversees more than $450 billion in assets under management.

The appetite for private market investments has been rising globally, driven by investors seeking portfolio diversification and stronger returns. This trend is further fueled by a slowdown in global capital market activity amid higher borrowing costs, with the alternative asset market projected to reach $30 trillion by the end of the decade.

Marwan Hadi, group head of retail and wealth management at Emirates NBD, said: “Innovation is a cornerstone at Emirates NBD, and we are pleased to partner with BlackRock to offer access to best-in-class, products in alternative markets through a dedicated platform while supporting the growing needs of investors in the region.”

He added: “We are deeply committed to creating value through our offerings and advancing the investment landscape in the UAE and the wider region, which has been experiencing a strong appetite in the last few years.”

This partnership also aims to democratize investment opportunities previously limited to institutional investors and ultra-high-net-worth individuals.

Beyond investment opportunities, BlackRock will leverage its open architecture approach to support Emirates NBD Asset Management’s private markets expansion, offering services including marketing, education, training, and technology.

“We are delighted to partner with Emirates NBD as they build out their private markets platform. Spurred by investor sentiment and facilitated by product innovation, technology, and regulatory advancements, wealth allocations to private markets are predicted to increase materially over the next five years,” said Rachel Lord, head of International at BlackRock.

Emirates NBD serves more than 9 million customers across 13 countries, holding 997 billion dirhams ($271 billion) in assets as of Dec. 31, 2024.

Pakistani finance chief calls for coalition of developing nations to push for fair trade, financial reform

- Muhammad Aurangzeb floated the proposal while addressing the Asia Annual Conference 2025, held in China

- He called for reforming the global sovereign debt system, with G20 and IMF supporting debt relief, financial justice

ISLAMABAD: Federal Minister for Finance and Revenue Muhammad Aurangzeb has proposed the formation of a global coalition of developing nations to collectively advocate for fair trade and better representation in international financial institutions, while criticizing the global economy as unequal, according to an official statement issued on Wednesday.

The finance chief made these remarks during his address at the Boao Forum for Asia Annual Conference 2025, held in China.

The forum, often referred to as the “Asian Davos,” is a high-level platform where leaders from government, business and academia across Asia and other continents gather to discuss pressing global and regional issues, with this year’s conference — titled “Asia in the Changing World: Towards a Shared Future” — running from March 25 to 28.

“Developing countries must unite to demand fair trade principles and improved representation in global financial institutions,” Aurangzeb said, according to a finance ministry statement, as they asked them to form a global coalition.

He said globalization’s had led to general progress, but its benefits remained unevenly distributed.

“The global economy has undoubtedly driven economic growth,” Aurangzeb said, according to a statement released by Pakistan’s finance ministry. “However, it remains highly unequal and fragmented.”

“Such an economy primarily benefits developed nations, while countries in the Global South are often overlooked,” he added.

Highlighting the structural challenges faced by developing nations, Aurangzeb pointed to high tariffs, discriminatory trade practices and barriers to market access that limit their ability to participate fully in the global economy.

He also stressed the urgency of reforming the global sovereign debt system, urging multilateral institutions such as the G20 and the IMF to play a more constructive role in debt relief and financial justice.

“The G20 and IMF must reform the sovereign debt system to enable debt forgiveness and ensure financial fairness,” he said.

Calling for inclusive and sustainable growth, Aurangzeb advocated for stronger multilateral cooperation to promote equitable market access, enhance regional connectivity, and build a global economy that works for all.

“An inclusive global economy is not a choice but a necessity,” he said.

He also underscored the role of technology in closing the global equity gap, recommending the creation of international AI and fintech funds to support digital inclusion in developing countries.

“Technology should serve as a tool for equity,” he said.

The finance minister further called for sustainability and environmental justice to be integrated into globalization policies.

He stressed the need for increased climate financing and easier technology transfer to countries most vulnerable to the effects of climate change.