NAIROBI: Uganda Airlines has taken to the skies once more after almost two decades out of action, but flies into a crowded aviation market in Africa where carriers have the weakest finances and emptiest planes of any region in the world.

The state carrier launched commercial flights on Wednesday, its first since it was liquidated in 2001, aiming to take a slice of the East African aviation business that is dominated by Ethiopian Airlines, the continent's success story.

Uganda is the latest African government to pour money into national flag carriers; Tanzania and Senegal are also resurrecting their airlines, while the likes of Rwanda, Ivory Coast and Togo are expanding theirs.

But such efforts have been hampered by high business costs as well as protectionism, which has impeded a continental open-skies agreement - something industry experts say is vital for the success of African carriers in a tough market.

The African market is forecast to grow almost 5% a year over the next two decades in terms of passengers, faster than mature markets, according to the International Air Transport Association (IATA). However, this is from a low base and most state-owned flag carriers in the region are losing money.

While the global aviation industry is on track to make a profit of $28 billion, African airlines are projected to make combined losses of $100 million this year, IATA said in June.

Uganda Airlines, like some of its rivals, aims to attract more domestic travellers to help it buck the gloomy continental trend. Around 2 million passengers per year travel through Entebbe, Uganda's main airport. Around 70% are Ugandans, said the carrier's CEO Ephraim Bagenda.

"All those currently travel on foreign airlines," he told Reuters. "We want part of that cake."

Last year, it looked like Africa was making progress on an open-skies agreement - the Single African Air Transport Market - to let airlines decide how frequently they fly between cities and which aircraft they use.

A total of 28 countries have signed up, accounting for 75-80% of African air traffic. Uganda is considering signing, Works and Transport Minister Monica Azuba Ntege said.

However, so far only 10 signatories - including Cape Verde, Ghana, Togo, Ethiopia and Nigeria - have begun changing their own laws to implement the deal and open up their markets, said Raphael Kuuchi, Vice President for Africa at IATA.

The patchy efforts undermine the agreement and hobble direct connections within Africa, say analysts. Some airlines, including from countries that have signed up, oppose the open-skies deal because they fear bigger competitors.

"The most subsidised airlines and the biggest ones are going to take the biggest market share because they (are) able to afford it," Kenya Airways CEO Sebastian Mikosz told an investor briefing on Tuesday. "They are going to kill the smaller national airlines which are just starting because they will have no way to defend themselves."

Ethiopian Airlines, sub-Saharan Africa's only successful large state-owned airline, has bucked the regional trend and has been expanding fast, thanks in part to having secured key traffic rights in two ways.

First, it signed bilateral agreements with nearly all African countries in the 1970s, activating them as needed, said Kuuchi. The airline flew to parts of the continent served by few other carriers and leveraged that goodwill to open up markets.

"Governments were willing to give them additional rights, and travel rights, once you give them out, it's very difficult to retract," he added.

More recently, Ethiopian has been helping other countries launch their own carriers and taking a stake. That has created regional continental hubs in Togo, Malawi and Chad where it can pick up and feed traffic into its main hub in Addis Ababa, cementing its dominance and rivalling Gulf carriers.

Now governments are hoarding travel rights to protect their own airlines, so African carriers are struggling to set up hubs vital to winning international travellers, said Girma Wake, former CEO of Ethiopian Airlines.

"Instead of flying point-to-point everywhere, if they can collect traffic from the low-traffic areas and bring them to major hubs and carry them from those major hubs, you will be in a better position," he told Reuters.

African aviation accounted for only 2.1% of the global market in 2018, with 92 million passenger journeys flown, and non-African airlines including Emirates and Turkish Airlines account for around 80% of traffic in and out of the continent, IATA said.

African airlines are also struggling to improve load factors - percentage of seats filled - from the world's lowest regional level of 71% in 2018, compared with 81.2% globally, according to IATA.

Emirates builds traffic through its global Dubai hub, an advantage most African airlines don't have - except Ethiopian Airlines.

As well as protectionism, high fuel and taxation hurt African carriers.

In Europe, a passenger can travel 1.5 hours for less than $100 all-inclusive. In Africa, passenger taxes alone range from $40 to $150 per passenger, African Airlines Association Secretary General Abderahmane Berthe told Reuters.

"Many governments are levying taxes on aviation and not reinvesting these collected amounts in aviation," he said.

Governments often see air transport as a luxury that can sustain high taxes, said Air Tanzania managing director Ladislaus Matindi.

Fuel is also taxed heavily and must often be trucked in, an expensive operation. Fuel makes up about a quarter of operating costs globally but reaches 30-40% in Africa, Berthe said.

Uganda Airlines, founded by former dictator Idi Amin in 1976, was liquidated in 2001 after years of unprofitability during a push to privatise state firms.

Other African state carriers have been crippled by government interference, such as insisting on routes to unprofitable but politically important destinations.

Ghana Airways, which ceased operations in 2005, used to fly between Accra and Las Palmas, mainly because of the friendship between the leaders of the two countries, IATA's Kuuchi said.

Uganda Airlines CEO Bagenda insisted his company would be free from any political interference.

"Government policy in Uganda is eyes on, hands off," he said.

Crowded African skies get even busier with Uganda Air’s return

Crowded African skies get even busier with Uganda Air’s return

- Continent lacks Dubai-style hub as Emirates and Turkish Airlines dominate routes

Saudi non-oil growth holds firm in March with PMI at 58: S&P Global

RIYADH: Saudi Arabia’s non-oil private sector maintained its resilience in March, with the Kingdom’s Purchasing Managers’ Index reaching 58.1, the highest among its Middle Eastern peers.

According to the latest Riyad Bank Saudi Arabia PMI report compiled by S&P Global, non-oil private firms in the Kingdom witnessed a marked increase in new order volumes, although the growth rate softened further from the near 14-year record seen in January.

The March figure represented a slight decline from the 58.4 seen in February, but it was still higher than UAE’s PMI rating of 54, Kuwait’s at 52.3 and Qatar’s at 52.

Any PMI reading above 50 signifies an expansion, while a reading below 50 indicates a contraction.

The sustained momentum reflects the Kingdom’s Vision 2030 strategy to reduce reliance on oil by accelerating growth in tourism, manufacturing, logistics, and financial services.

Naif Al-Ghaith, chief economist at Riyad Bank, described the Saudi non-oil private sector as demonstrating “significant resilience and growth,” adding: “This reading reflects sustained positive momentum in business conditions, highlighting the sector’s robust economic health and its vital role in the ongoing diversification efforts of the Kingdom as envisaged by Vision 2030.”

Saudi Arabia’s non-oil businesses continued to increase their employment at an elevated pace in March, driven by an upturn in demand.

The report further said that staffing growth was little changed from February’s 16-month high, as firms widely commented on efforts to build their sales teams and overall capacity.

Survey data also indicated that job growth in Saudi Arabia’s non-oil private sector during the first three months of this year was the fastest since the third quarter of 2012.

“Rising employment rates are a direct benefit of businesses scaling up operations to meet demand. By providing more job opportunities, Saudi Arabia aims to nurture a skilled and ambitious workforce, reducing the unemployment rate to 7 percent for Saudi nationals,” said Al-Ghaith.

Speaking at the World Investment Conference in Riyadh last November, Saudi Arabia’s Minister of Economy and Planning Faisal Al-Ibrahim said non-oil activities now account for 52 percent of the Kingdom’s gross domestic product. He added that the non-oil economy has grown by 20 percent since the launch of Vision 2030.

The latest PMI report added that greater marketing efforts, lower selling prices, and a broader improvement in economic conditions played a crucial role in driving sales growth among non-oil firms in Saudi Arabia in March.

New orders from foreign markets also rose in March, although the rate of expansion slowed.

Highlighting the affinity of Saudi Arabia’s non-oil products in international markets, a report by the General Authority for Statistics revealed that the Kingdom’s non-energy exports surged by 10.7 percent in January to reach SR26.48 billion ($7.06 billion).

According to the latest S&P Global report, increased workforces and stronger new businesses supported a robust upturn in non-oil private sector activity during March.

Non-oil firms in the Kingdom also engaged in additional stockpiling as they anticipate a sustained uplift in sales.

Companies that took part in the survey revealed that purchasing activity rose sharply in March, leading to another steep increase in total inventories.

“The improvement in business conditions supports efforts to attract investment, increase the competitiveness of the Saudi economy, and enhance local business growth,” said Al-Ghaith.

He added: “This initiative is further supported by governmental enhancements in regulatory frameworks and infrastructure investments which pave the way for greater private and foreign investments.”

Attracting international investments is one of the crucial goals outlined in Saudi Arabia’s Vision 2030, with the Kingdom aiming to attract $100 billion a year in foreign direct investment by the end of this decade.

The latest S&P Global report further said that suppliers’ delivery times improved in March, with several panellists noting that strong vendor relationships had facilitated efficiency gains.

However, some reports of supply disruption and administrative delays led to a much softer overall upturn in performance compared to February. This softening also hindered efforts to clear outstanding work, contributing to a renewed and sharp rise in total backlogs.

In terms of pricing, the latest survey revealed that input cost pressures witnessed a marked easing in March.

The report added that the rate of inflation dropped to its lowest level in just over four years, as firms saw a much weaker increase in purchase prices. Consequently, non-oil companies reduced their selling prices for the first time in six months.

“Sustaining and nurturing these positive trends, Saudi Arabia is laying the groundwork for a multifaceted and thriving economy that meets the aspirations of its people and the strategic goals of the nation,” said Al-Ghaith.

“With each uptick in the PMI and every incremental GDP growth, the Kingdom moves closer to realizing its ambitions of a diversified, sustainable economic future,” he concluded.

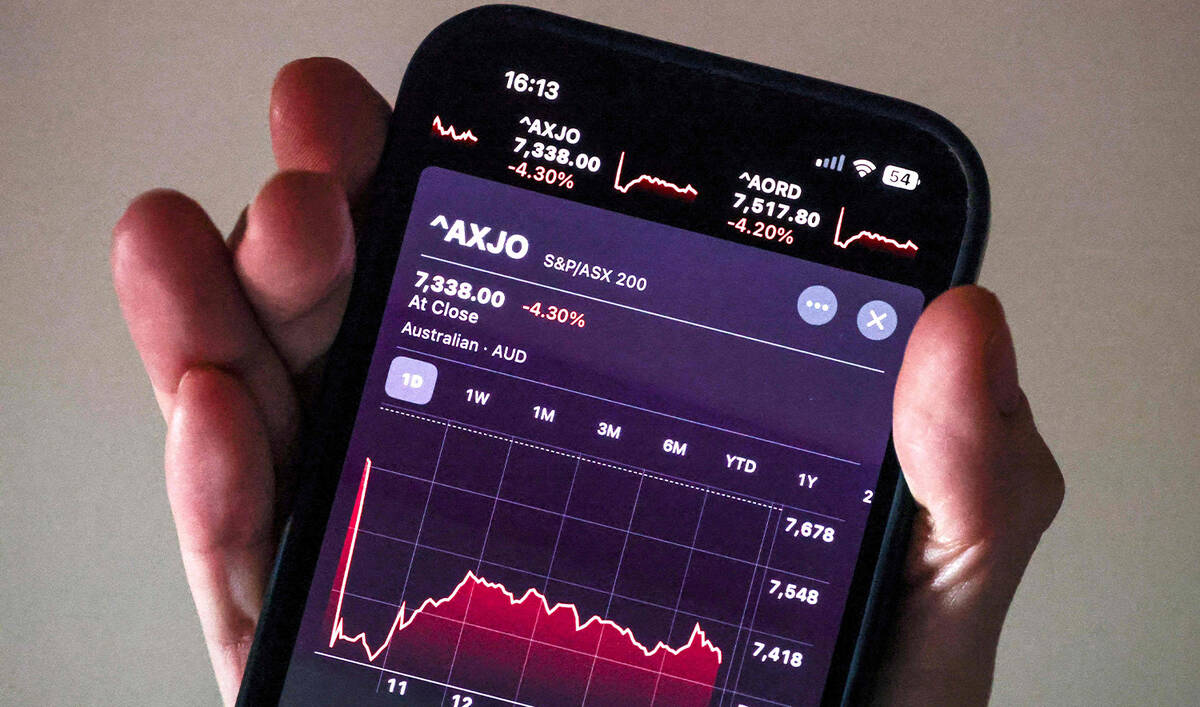

Global markets fall as Trump’s tariffs roil world trade

- Pakistan Stock Exchange falls rapidly, suspending trading for an hour after a 5% drop in KSE-100 index

- Middle East stock markets tumble as they struggled with dual hit of new US tariffs, oil prices decline

Global markets plunged Monday following last week’s two-day meltdown on Wall Street, and President Donald Trump said he won’t back down on his sweeping new tariffs, which have roiled global trade.

Countries are scrambling to figure out how to respond to the tariffs, with China and others retaliating quickly.

Trump’s tariff blitz fulfilled a key campaign promise as he acted without Congress to redraw the rules of the international trading system. It was a move decades in the making for Trump, who has long denounced foreign trade deals as unfair to the US

The higher rates are set to be collected beginning Wednesday, ushering in a new era of economic uncertainty with no clear end in sight.

Here’s the latest:

Chinese officials meet business representatives from Tesla and other US companies.

Chinese government officials met business representatives from Tesla, GE Healthcare and other US companies on Sunday. It called on them to issue “reasonable” statements and take “concrete actions” on addressing the issue of tariffs.

“The United States in recent days has used all sorts of excuses to announce indiscriminate tariffs on all trading partners, including China, severely harming the rules-based multilateral trade system,” said Ling Ji, a vice minister of commerce, at the meeting with 20 US companies.

“China’s countermeasures are not only a way to protect the rights and interests of companies, including American ones, but are also to urge the US to return to the right path of the multilateral trading system,” Ling added.

Ling also promised that China would remain open to foreign investment, according to a readout of the meeting from the Ministry of Commerce.

Malaysia wants Southeast Asia to present a united response to tariffs

Malaysia’s Trade Minister Zafrul Abdul Aziz said his country wants to forge a united response from Southeast Asia to the sweeping US tariffs.

Malaysia, which is the chair of the Association of Southeast Asian Nations this year, will lead the regional bloc’s special Economic Ministers’ Meeting on April 10 in Kuala Lumpur to discuss the broader implication of the tariff measures on regional trade and investment, Zafrul told a news conference on Monday.

“We are looking at the investment flow, macroeconomic stability and ASEAN’s coordinated response to this tariff issue,” Zafrul said.

ASEAN leaders will also meet to discuss member states’ strategies and to mitigate potential disruptions to regional supply chain networks.

Pakistan plans to send a government delegation to Washington this month to discuss how to avoid the 29% tariffs imposed by the US on imports from Pakistan, officials said Monday.

The development came two days after Pakistan’s prime minister asked its finance minister to send him recommendations for resolving the issue. The US imports around $5 billion worth of textiles and other products from Pakistan, which heavily relies on loans from the International Monetary Fund and others.

The Pakistan Stock Exchange fell rapidly on Monday. The exchange suspended trading for an hour after a 5% drop in its main KSE-30 index.

Mideast markets follow oil prices lower

Middle East stock markets tumbled as they struggled with the dual hit of the new US tariffs and a sharp decline in oil prices, squeezing energy-producing nations that rely on those sales to power their economies and government spending.

Benchmark Brent crude is down by nearly 15% over the last five days of trading, with a barrel of oil costing just over $63. That’s down nearly 30% from a year ago, when a barrel cost over $90.

That cost per barrel is far lower than the estimated break-even price for producers. That’s coupled with the new tariffs, which saw the Gulf Cooperation Council states of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates hit with 10% tariffs. Other Mideast nations face higher tariffs, like Iraq at 39% and Syria at 41%.

The Dubai Financial Market exchange fell 5% as it opened for the week. The Abu Dhabi Securities Exchange fell 4%.

Markets that opened Sunday saw losses as well. Saudi Arabia’s Tadawul stock exchange fell over 6% in trading. The giant of the exchange, Saudi Arabia’s state-owned oil company Aramco, fell over 5% on its own, wiping away billions in market capitalization for the world’s sixth-most-valuable company.

Beijing struck a note of confidence on Monday even as markets in Hong Kong and Shanghai tumbled.

“The sky won’t fall. Faced with the indiscriminate punches of US taxes, we know what we are doing and we have tools at our disposal,” wrote The People’s Daily, the Communist Party’s official mouthpiece.

China announced a slew of countermeasures on Friday evening aimed at Trump’s tariffs, including its own 34% tariffs on all goods from the US set to go in effect on Wednesday.

Australian dollar drops to levels last seen early in pandemic

The Australian dollar fell below 60 US cents on Monday for the first time since the early months of the COVID-19 pandemic.

The drop reflected concerns over the Chinese economy and market expectations for four interest rate cuts in Australia this calendar year, Australian Treasurer Jim Chalmers said.

“What our modeling shows is that we expect there to be big hits to American growth and Chinese growth and a spike in American inflation as well,” Chalmers said.

“We expect more manageable impacts on the Australian economy, but we still do expect Australian GDP to take a hit and we expect there to be an impact on prices here as well,” he added.

The Trump administration assigned Australia the minimum baseline 10% tariff on imports in the United States. The US has enjoyed a trade surplus with Australia for decades.

Indian stocks fell sharply on Monday, seeing their biggest single-day drop in percentage terms since March 2020 amid the pandemic.

The benchmark BSE Sensex and the Nifty 50 index both dropped about 5% after trading opened but then recovered slightly. Both were later trading down about 4 percent.

President Donald Trump said Sunday that he won’t back down on his sweeping tariffs on imports from most of the world unless countries even out their trade with the US, digging in on his plans to implement the taxes that have sent financial markets reeling, raised fears of a recession and upended the global trading system.

Speaking to reporters aboard Air Force One, Trump said he didn’t want global markets to fall, but also that he wasn’t concerned about the massive sell-off either, adding, “sometimes you have to take medicine to fix something.”

His comments came as global financial markets appeared on track to continue sharp declines once trading resumes Monday, and after Trump’s aides sought to soothe market concerns by saying more than 50 nations had reached out about launching negotiations to lift the tariffs.

“I spoke to a lot of leaders, European, Asian, from all over the world,” Trump said. “They’re dying to make a deal. And I said, we’re not going to have deficits with your country. We’re not going to do that, because to me a deficit is a loss. We’re going to have surpluses or at worst, going to be breaking even.”

Asian markets plunged on Monday following last week’s two-day meltdown on Wall Street, and US President Donald Trump said he won’t back down on his sweeping tariffs on imports from most of the world unless countries even out their trade with the US

Tokyo’s Nikkei 225 index lost nearly 8% shortly after the market opened on Monday. By midday, it was down 6%. Hong Kong’s Hang Seng dropped 9.4%, while the Shanghai Composite index was down 6.2%, and South Korea’s Kospi lost 4.1%

US futures also signaled further weakness.

Market observers expect investors will face more wild swings in the days and weeks to come, with a short-term resolution to the trade war appearing unlikely.

Oil Updates — crude tumbles further as US-China trade tensions fuel recession fears

LONDON : Oil prices extended last week’s losses on Monday, with West Texas Intermediate falling more than 4 percent, as escalating trade tensions between the US and China stoked fears of a recession that would reduce demand for crude.

Brent futures declined $2.54, or 3.9 percent, to $63.04 a barrel at 10:45 a.m. Saudi time, while US WTI crude futures lost $2.5, or 4.03 percent, to $59.49. Both benchmarks dropped their lowest since April 2021.

Oil plunged 7 percent on Friday as China ramped up tariffs on US goods, escalating a trade war that has led investors to price in a higher probability of recession. Last week, Brent lost 10.9 percent, while WTI dropped 10.6 percent.

“It’s hard to see a floor for crude unless the panic in the markets subsides and it’s hard to see that happening unless Trump says something to arrest snowballing fears over a global trade war and recession,” said Vandana Hari, founder of oil market analysis provider Vanda Insights.

Responding to US President Donald Trump’s tariffs, China said on Friday it would impose additional levies of 34 percent on American goods, confirming investor fears that a full-blown global trade war is underway.

Imports of oil, gas and refined products were given exemptions from Trump’s sweeping new tariffs, but the policies could stoke inflation, slow economic growth and intensify trade disputes, weighing on oil prices.

Federal Reserve Chair Jerome Powell said on Friday that Trump’s new tariffs are “larger than expected,” and the economic fallout, including higher inflation and slower growth, likely will be as well.

Adding to the price changes, the Organization of the Petroleum Exporting Countries and allies decided to advance plans for output increases. The group now aims to return 411,000 barrels per day to the market in May, up from the previously planned 135,000 bpd.

“This potential influx of supply, reversing cuts maintained over the past two years, represents a major shift in market dynamics and acts as a significant headwind for prices,” said Sugandha Sachdeva, founder of SS WealthStreet, a New Delhi-based research firm.

Over the weekend, top OPEC+ ministers stressed the need for full compliance with oil output targets and called for overproducers to submit plans by April 15 to compensate for pumping too much.

On the geopolitical front, Iran on Sunday rejected US demands that it hold direct nuclear talks or face strikes. Russia claimed to have captured Basivka in Ukraine’s Sumy region and said its forces were attacking multiple nearby settlements.

Riyadh Air receives Air Operator Certificate, set to launch flights in 2025

RIYADH: Saudi Arabia’s Riyadh Air has received approval from the General Authority of Civil Aviation to commence its flight operations, according to a statement released on Sunday.

The airline, owned by the Public Investment Fund, was granted the Air Operator Certificate after successfully meeting all regulatory, safety, and operational standards.

This milestone aligns with Riyadh Air’s goal of connecting over 100 international cities by 2030 and contributing more than $20 billion to the Kingdom’s economy.

Additionally, the airline aims to enhance the travel experience by leveraging digital technology to streamline bookings and airport procedures, catering to Saudi Arabia’s young, tech-savvy population, as highlighted by CEO Tony Douglas.

During the certificate delivery ceremony, Saudi Minister of Transport and Logistics Saleh Al-Jasser told Al-Ekhbariya: “We congratulate Riyadh Air, the Public Investment Fund, and the Saudi citizens on the successful completion of the licensing process and the official issuance of the Air Operator Certificate.”

He further emphasized that Riyadh Air is now fully certified to operate, marking a significant milestone in the initiative set in motion by Crown Prince Mohammed bin Salman’s strategy, which tasked PIF with launching the carrier.

“Establishing an airline of this scale is a monumental task, but the process is progressing smoothly. We are now in the final stages, with the next step being the launch of the first flight before the end of this year,” the minister remarked.

Al-Jasser also highlighted that the Kingdom is in the midst of restructuring its aviation infrastructure and launching several initiatives aimed at advancing the country’s aviation sector.

“The transport strategy includes restructuring the aviation sector, transitioning from a single operator model to a multi-operator system,” he said.

The minister added: “King Salman International Airport Development Co. is making steady progress in finalizing the airport’s design, with construction already underway. This comprehensive project includes passenger terminals, runways, private aviation facilities, and technical services, creating a fully integrated aviation city that is being developed as planned.”

Al-Jasser further noted that development projects are ongoing at airports in Jazan, Hail, and Qassim, as well as in Al-Baha, Abha, Taif, and Al-Jouf.

“Saudi airports have made significant strides in regulations, legislation, and services, which have attracted investments, strengthened passenger rights, and enhanced service quality,” he said.

The minister also emphasized: “We’ve expanded from 100 destinations connected to the Kingdom’s airports to 172 destinations, with the aviation strategy being a comprehensive plan for the future.”

Saudi Aramco cuts oil prices to Asia to four-month low

RIYADH: Saudi Aramco on Sunday cut its crude oil prices for Asian buyers in May to their lowest in four months, an official document showed.

This is the second consecutive month Aramco has lowered its prices. The company also lowered April prices for other grades it sells to Asia by $2.30 per barrel.

Aramco cut the May official selling price for flagship Arab Light crude by $2.30 to $1.20 a barrel above the average of Oman and Dubai prices, a pricing document from the producer showed.

The company also lowered April prices for other grades it sells to Asia by $2.30 per barrel.

Eight OPEC+ countries unexpectedly agreed on Thursday to advance their plan to phase out oil output cuts by increasing output by 411,000 barrels per day in May, a decision that prompted oil prices to extend earlier sharp losses.

Prior to the news, Arab Light price for Asia had been expected to fall by $1.80 to $2 in a Reuters survey, tracking the steep declines in benchmark prices in March.

Saudi Aramco’s crude oil is classified into five grades based on density: Super Light (greater than 40), Arab Extra Light (36-40), Arab Light (32-36), Arab Medium (29-32), and Arab Heavy (below 29). These price changes influence the cost of approximately 9 million barrels per day of crude oil shipped to Asia, setting price benchmarks for other major oil producers such as Iran, Kuwait, and Iraq.

For North America, Aramco has set the May OSP for Arab Light crude at $3.60 per barrel above the Argus Sour Crude Index.

Spot premium of Dubai averaged at $1.38 per barrel in March, down from $3.33 per barrel, the average in February following more Russian supply returning to Asia since March.